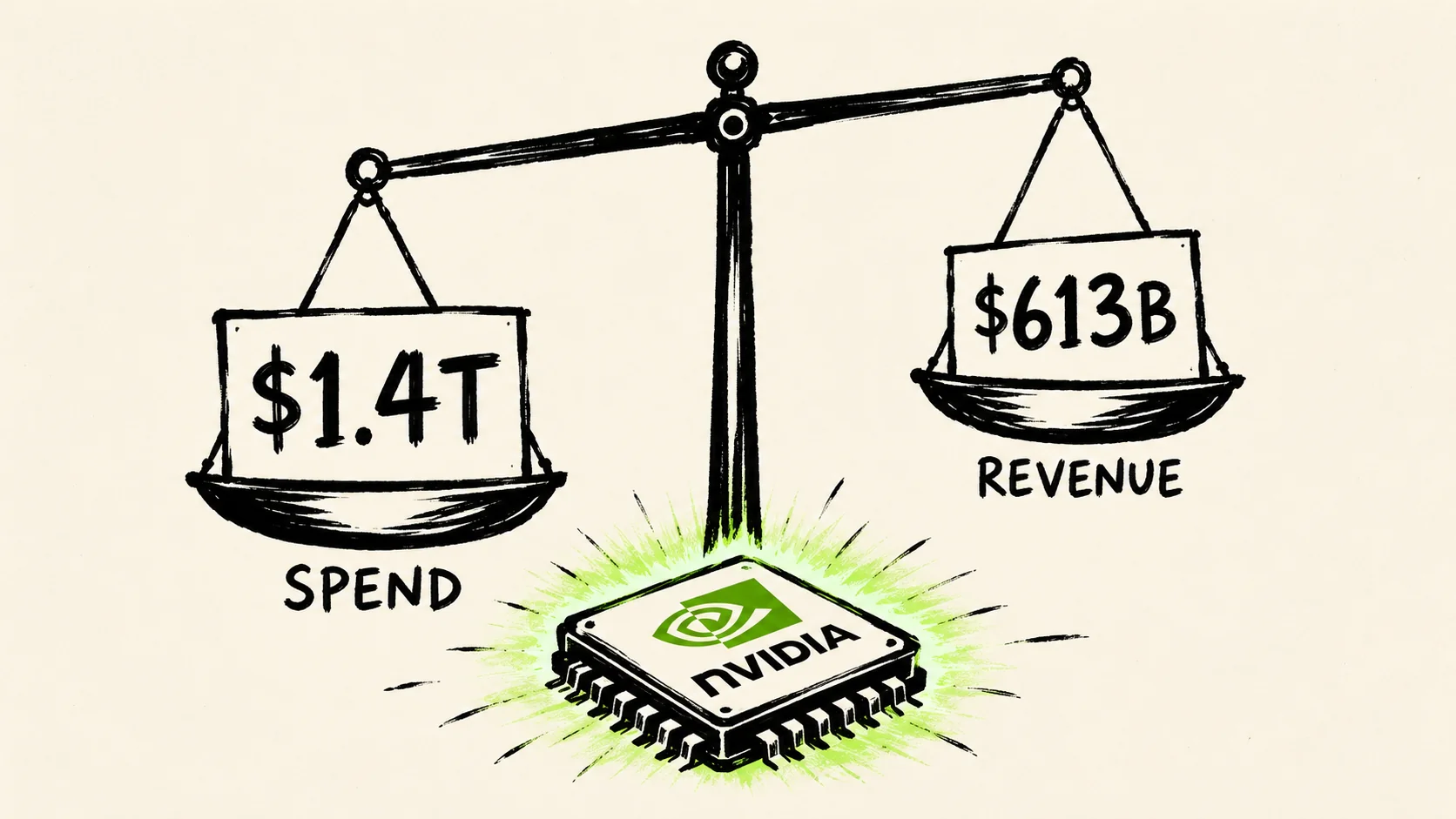

The aggregate financial picture for frontier AI through May 2026 is straightforward: the industry has deployed an estimated $1.4 trillion in capital and recovered approximately $613 billion in revenue, leaving a cumulative net loss of roughly $787 billion. One company, Nvidia, accounts for nearly all of the sector's profit.

Big Tech Has Committed Over $1 Trillion in AI Capex With Revenue Lagging Sharply

Amazon, Alphabet, Microsoft, Meta, and Oracle together account for roughly $1.15 trillion of the industry's total estimated capital expenditure since 2022. In every case, revenue attributed to AI operations trails spend by a wide margin — and in Meta's case, by an extraordinary one.

Amazon's cumulative AI-related capex since 2022 is estimated at $313 billion, the largest single commitment in the cohort. AI revenue for that period is estimated at $22 billion, almost entirely channeled through AWS infrastructure. The company signaled its spend trajectory when it confirmed plans to deploy $100 billion in capex in 2025 alone, with the majority directed at AI workloads. Alphabet's capex figure sits at roughly $287 billion since 2022, with AI-attributable cloud revenue estimated at approximately $25 billion — about 40% of its total cloud segment, an allocation that is itself an analyst estimate rather than a separately reported line item. Microsoft, which confirmed a $37 billion annual run rate for AI revenue in May 2026, has deployed an estimated $266 billion in AI-related capex since 2022 while recognizing approximately $31 billion in cumulative AI revenue.

Meta presents a structurally different case. Its cumulative AI capex is estimated at $230 billion, yet direct AI product revenue is estimated at only $3 billion, because Llama is distributed as open-source software and Meta AI is embedded at no charge into its consumer platforms. The company is not attempting to monetize AI directly — a deliberate choice that makes its PNL figure of roughly -$227 billion appear larger than its commercial peers without being an equivalent strategic failure.

One important caveat applies across this entire segment: the capital flows are partly circular. Amazon and Google have both invested in Anthropic; Microsoft co-invests with OpenAI. When those labs spend their funding on cloud compute, a portion of the Big Tech capex and the Big Tech AI revenue in this tracker are recording the same dollars twice — once as a venture commitment and again as cloud consumption. That circularity means the true net industry loss is likely smaller than the aggregate figures suggest, though by how much is not independently verifiable from public disclosures.

The chart below compares cumulative estimated capex against estimated AI revenue for each Big Tech participant, illustrating how wide the spending gap remains.

OpenAI, Anthropic, and xAI Are Burning Cash at Very Different Rates

The three highest-profile pure-play AI research labs share a common condition — none is profitable — but their spending efficiency and revenue trajectories diverge significantly.

OpenAI carries the heaviest loss position. Internal documents cited by Fortune project cumulative losses of $44 billion across 2023 through 2028, with a net loss of approximately $14 billion expected for 2026 alone. Yahoo Finance reported the same internal forecast, noting that the company's monthly revenue has reached $2 billion — an annualized pace of roughly $24 billion. Against an estimated cumulative spend of $55 billion since 2020 and cumulative revenue of $28 billion, OpenAI's running PNL stands at approximately -$27 billion.

Anthropic's financial profile is structurally tighter. Its estimated cumulative spend since 2021 is $33 billion — roughly 60% of OpenAI's — against $6.5 billion in cumulative recognized revenue, for a PNL of approximately -$26.5 billion. Industry analysts noted in early 2026 that Anthropic had achieved a higher revenue-to-training-cost ratio than OpenAI, spending substantially less per model generation. Anthropic also reported a $30 billion annual recurring revenue figure by April 2026, representing contracted enterprise commitments — though ARR is a forward-looking run-rate construct and the cumulative recognized revenue of $6.5 billion reflects what has been billed and collected to date, not what is under contract. Those two numbers are tracking different things. Anthropic's broader enterprise push suggests the company is prioritizing developer infrastructure as a revenue moat.

xAI, founded in 2023, is spending at an estimated $1 billion per month. With cumulative spend of approximately $20 billion and revenue of roughly $0.8 billion, its cumulative PNL sits at -$19.2 billion. xAI's runway and path to revenue scale are not publicly disclosed beyond burn-rate estimates.

The chart below shows the spend-versus-revenue gap for each of the three major pure-play labs.

DeepSeek's Training Cost Figures Expose How Much Efficiency Varies Across the Industry

While the major Western labs are spending tens of billions, DeepSeek has demonstrated that certain frontier-capable models can be produced at a fraction of that cost — though the comparison requires careful framing.

A peer-reviewed paper published in Nature, reported by MLQ.ai, confirmed that DeepSeek's R1 model cost approximately $294,000 to train. That figure covers only the final training run for R1, not the full infrastructure cost. The underlying V3 base model — which R1 builds on — cost an additional $6 million to develop. Even with the full stack, the combined figure of roughly $6.3 million is orders of magnitude below what OpenAI or Anthropic spend on equivalent development cycles.

DeepSeek's cumulative spend since 2023 is estimated at just $300 million, against approximately $100 million in recognized revenue — a PNL of roughly -$200 million. Despite this, the company reportedly reached a $220 million annual recurring revenue pace by mid-2025 and is targeting a $45 billion valuation in its first external investment round as of May 2026.

Mistral AI and Cohere sit in a similar mid-tier efficiency band. Mistral has spent an estimated $1 billion since 2023 against $400 million in revenue; Cohere has spent $700 million since 2020 against $400 million in revenue. Both remain loss-making, but their PNL gaps are manageable relative to frontier-scale peers.

The efficiency contrast matters because it signals that the cost structure of AI development is not uniform. The large capex figures in the Big Tech segment and at OpenAI reflect choices about scale and capability targets, not a fixed industry floor. The metric cards below compare the key efficiency signals from the lower-cost segment.

Nvidia Is the Sector's Only Net-Positive Participant at Scale

Every major AI development organization is spending more than it earns from AI. Nvidia is not.

As the dominant supplier of GPU hardware to the entire sector — including to Amazon, Google, Microsoft, Meta, Oracle, OpenAI, and Anthropic — Nvidia occupies a position that is structurally separate from the rest of the industry's financial picture. Its chips are the infrastructure layer on which the losses of every other participant run.

Since 2023, Nvidia's estimated cumulative revenue has reached approximately $478 billion against $225 billion in costs, yielding an estimated cumulative profit of +$253 billion. That figure is not an allocation or an analyst estimate in the same way the AI sub-segment figures are — Nvidia reports its data center revenue directly as a single reported business unit, making it the most verifiable number in this tracker.

The implication is structural: the industry's capital flows toward Nvidia from all directions simultaneously. When Amazon buys servers for AWS, when Google funds another Gemini training run, when OpenAI scales its inference fleet, and when Anthropic expands its model development capacity, Nvidia collects revenue from each transaction. The company is not betting that AI will generate returns — it is collecting returns now, while the rest of the industry makes that bet.

The chart below shows the cumulative PNL divergence between Nvidia and the industry aggregate, illustrating the structural asymmetry.

The $787 billion aggregate loss figure carries a significant caveat: because the same dollars often flow from a cloud provider's venture arm into a lab and then back to that cloud provider as compute spend, the true net industry loss is overstated by an amount that cannot be precisely quantified from public disclosures. What the figure does capture accurately is the direction and scale of the industry's financial position — and the fact that Nvidia, alone among major participants, is collecting more than it is spending.

The Retirement Countdown: What to Fix at 5 Years, 3 Years and 1 Year Out

Retirement checklist: what advisors say to fix at 5, 3 and 1 year out — Social Security claiming order, IRA withdrawal sequencing and a 2028 tax deadline.

UnitedHealth's Adjusted EPS of $6.38 Beats Estimates by 30% as It Sheds Members for Margin

UnitedHealth posted $6.38 adjusted EPS in Q2 2026, beating estimates by 30%, as medical costs eased to 86.7% and full-year guidance rose to $19.50–$20.00.

Why SaaS Companies Fail: What the 2024 Shutdown Data Shows

CB Insights' 2024 study of 431 failed startups found 43% cite poor product-market fit; Carta data shows enterprise SaaS led 2024's shutdown wave at 32%.

Valuations Are Nearing Dot-Com Peaks: Is a 2026 Market Crash Imminent?

The S&P 500's Shiller CAPE ratio hit 41.76 and the Buffett Indicator sits near 214%, levels unseen since just before 2000 — here's what history suggests next.

Comments (0)

Please sign in to join the discussion.

No comments yet.

Be the first to share your perspective on this topic.