SpaceX has tapped Goldman Sachs as the lead-left bank on what could become the largest initial public offering in history, with the company targeting a Nasdaq debut as early as June 12 under the ticker "SPCX" and a valuation that sources place between $1.75 trillion and $2 trillion.

Goldman and Morgan Stanley Anchor a Wall Street Lineup Assembled for a Historic Raise

The lead-left position on a prospectus cover is the most commercially significant slot in any IPO bank lineup — it signals primary responsibility for book-building, carries the largest share of underwriting fees, and anchors investor confidence in the deal's structure. SpaceX awarded that position to Goldman Sachs, with Morgan Stanley taking the next slot, according to Bloomberg and CNBC reporting citing sources familiar with the matter.

Bank of America, Citigroup, and JPMorgan Chase appear on the preliminary prospectus in alphabetical order — a standard arrangement for secondary lead banks that avoids signaling a strict hierarchy among them. Deutsche Bank and UBS are positioned to handle European order coordination, while Barclays will oversee UK distribution.

SpaceX is targeting a preliminary prospectus filing as early as mid-May 2026. If the raise lands within the $75 billion to $80 billion range the company is reportedly seeking, it would shatter Saudi Aramco's 2019 record of $29.4 billion by a factor of roughly 2.5. Both Bloomberg and CNBC note that bank alignments and final deal parameters remain fluid; no terms have been formally filed with the SEC.

The chart below maps the reported bank hierarchy from lead-left anchor to regional distribution roles.

A Valuation Built Through Corporate Combinations, Not Organic Growth Alone

The $1.75–$2 trillion target valuation did not emerge from SpaceX's launch and satellite businesses in isolation. It reflects a sequence of corporate combinations that Elon Musk orchestrated in the months before the filing, each of which folded additional asset value into the SpaceX entity.

In February 2026, SpaceX merged with Musk's AI startup xAI at a reported combined valuation of $1.25 trillion. That deal was followed by SpaceX absorbing X (formerly Twitter) and acquiring the coding-assistant startup Cursor for $60 billion. The company also reportedly landed satellite data and computing power leases with Anthropic, adding a contracted revenue dimension. Shareholders approved a 5-for-1 stock split during the week of May 18, adjusting the internal fair market value from $526.59 to $105.32 per share — a standard pre-IPO step to improve retail accessibility and market float.

What this means in practice: analysts and investors assessing the $2 trillion headline must disaggregate which portions of valuation are attributable to SpaceX's core launch and Starlink revenues, which stem from xAI's AI model business, which reflect X's advertising and subscription base, and which derive from Cursor and the Anthropic arrangement. None of those component valuations have been disclosed separately in a filed document, and the sources do not provide individual segment revenue breakdowns. The number is a consolidated thesis, not a sum-of-parts disclosure.

The chart below shows the reported valuation trajectory across each combination event.

The Hedge Funds That Got In Early and What Their Stakes May Be Worth

Two private funds stand out among SpaceX's early institutional backers for the scale of their reported unrealized positions.

Darsana Capital Partners, a New York hedge fund founded by Anand Desai in 2014, first invested in SpaceX in 2019 when the company was valued at $33 billion. The fund subsequently added to its position through employee tender offers and held a pre-existing stake in X before that entity was absorbed into SpaceX. According to the Wall Street Journal, Darsana's combined stake could generate a windfall of more than $10 billion at the low end of the IPO valuation range, and potentially up to $15 billion if the $1.75 trillion figure is realized.

D1 Capital Partners, led by Dan Sundheim, first backed SpaceX in 2020 at a $36 billion valuation. The fund held its position despite significant inbound interest in purchasing the shares. Its stake is reported as potentially worth roughly $20 billion at listing.

Neither fund has publicly disclosed the size of its position. The lock-up period terms that would govern when these stakes can be sold following the IPO have not been confirmed, according to the sources reviewed. That detail matters considerably: a long lock-up at a volatile post-listing price introduces a gap between a paper windfall and a realized one.

BlackRock has held discussions about anchoring the listing with an investment between $5 billion and $10 billion, which would represent a demand signal from the institutional side rather than an early-backer windfall.

Separately, California's tax position is notable. Although SpaceX's formal headquarters are in Texas — which has no state income tax — a significant portion of its veteran workforce remains in California, which taxes capital gains as ordinary income at rates up to 13.3%. The equity cash-outs from early employees and fund investors with California tax exposure would generate a concentrated capital gains windfall for the state.

The chart below compares the reported entry valuations for Darsana and D1 against their projected stake values at IPO, illustrating the scale of the potential multiple.

SpaceX has not commented publicly on the IPO timeline or bank selection. The deal remains subject to market conditions, regulatory review, and final pricing negotiations. If the filing proceeds on the reported mid-May schedule and the June 12 debut holds, Wall Street will have a matter of weeks to absorb what would be the most heavily watched equity offering since Saudi Aramco — and a fundamentally different kind of company underneath the record-breaking numbers. Those watching how recent market conditions and April 2026 jobs data affect institutional risk appetite will find the demand picture for a $2 trillion ask a useful test of where that appetite actually sits.

Related Stories

Google and Blackstone Form TPU Cloud Joint Venture

Google and Blackstone's joint venture will create an independent AI cloud company offering Google TPU compute-as-a-service to enterprise customers, with 500MW of data center capacity targeted by 2027.

Samsung Strike Talks Resume With May 21 Deadline Hours Away

Samsung Electronics and its largest union resumed government-mediated pay talks on May 18, 2026, three days before a threatened 18-day strike by up to 50,000 workers that JPMorgan estimates could cost 2.1–3.5 trillion KRW in operating profit.

Markets Surge While Economy Strains: May 2026

U.S. stock markets climbed back to record territory in May 2026 even as crude oil hovers near $110, wholesale inflation runs at 6%, and bond yields signal the Fed's rate-cut path may be closing.

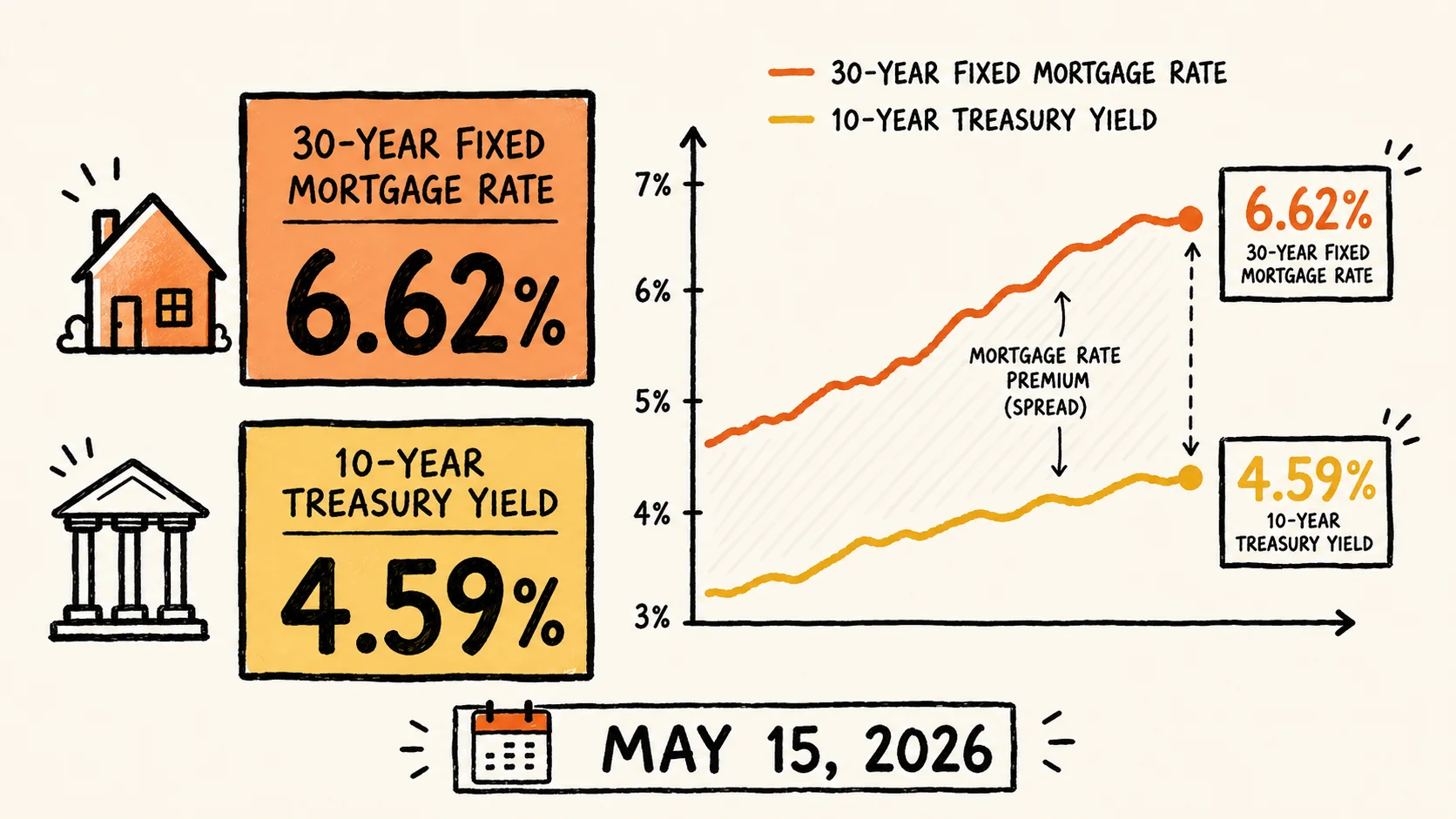

Mortgage Rates Hit 8-Month High at 6.62% — May 2026

Average 30-year fixed mortgage rates hit 6.62% on May 15, 2026, matching levels last seen in August 2025, driven by a 4.59% Treasury yield, 3.8% inflation, and a bond sell-off following the Trump-Xi summit.

Comments (0)

Please sign in to join the discussion.

No comments yet.

Be the first to share your perspective on this topic.