For three years, major AI platforms built their user bases on a simple but structurally unsound premise: charge less than it costs to serve, attract enough demand to justify the next round of capital, and figure out the margin problem later. That reckoning has now arrived — and the first people to feel it are the corporate customers who planned their budgets around the old pricing.

The Token-Maxxing Math That Made the Model Impossible

The clearest way to understand the structural problem is through what analysts and business media began calling "token-maxxing" — the practice of users maximizing consumption against a flat subscription price. According to testing documented by SemiAnalysis and cited in a June 2026 analysis by David Rosenthal, an enterprise subscriber paying $200 per month could burn through approximately $8,000 worth of compute on Anthropic or up to $14,000 on OpenAI. That translates to an implicit platform subsidy of roughly 40 times and 70 times the subscription price, respectively.

The cost-side picture is comparably stark. Estimates across the sourced material suggest platforms were spending between $8 and $14 for every $1 of revenue they collected. Even under an optimistic scenario — tokens priced at four times their generation cost — a user consuming just 25 percent of their rate limit pushes the platform into a negative gross margin position of around 25 percent, as Rosenthal's analysis describes.

David Cahn of Sequoia Capital identified the structural tension early. In September 2023, he estimated a $200 billion revenue gap between what AI infrastructure was costing and what the market was actually generating. By June 2024 he revised that figure to $600 billion — not because the underlying math had changed but because the capital deployment had accelerated faster than any credible revenue trajectory could support.

The chart below shows the subsidy multiples and cost ratios from sourced estimates, illustrating the gap between what platforms charged and what serving those subscriptions cost.

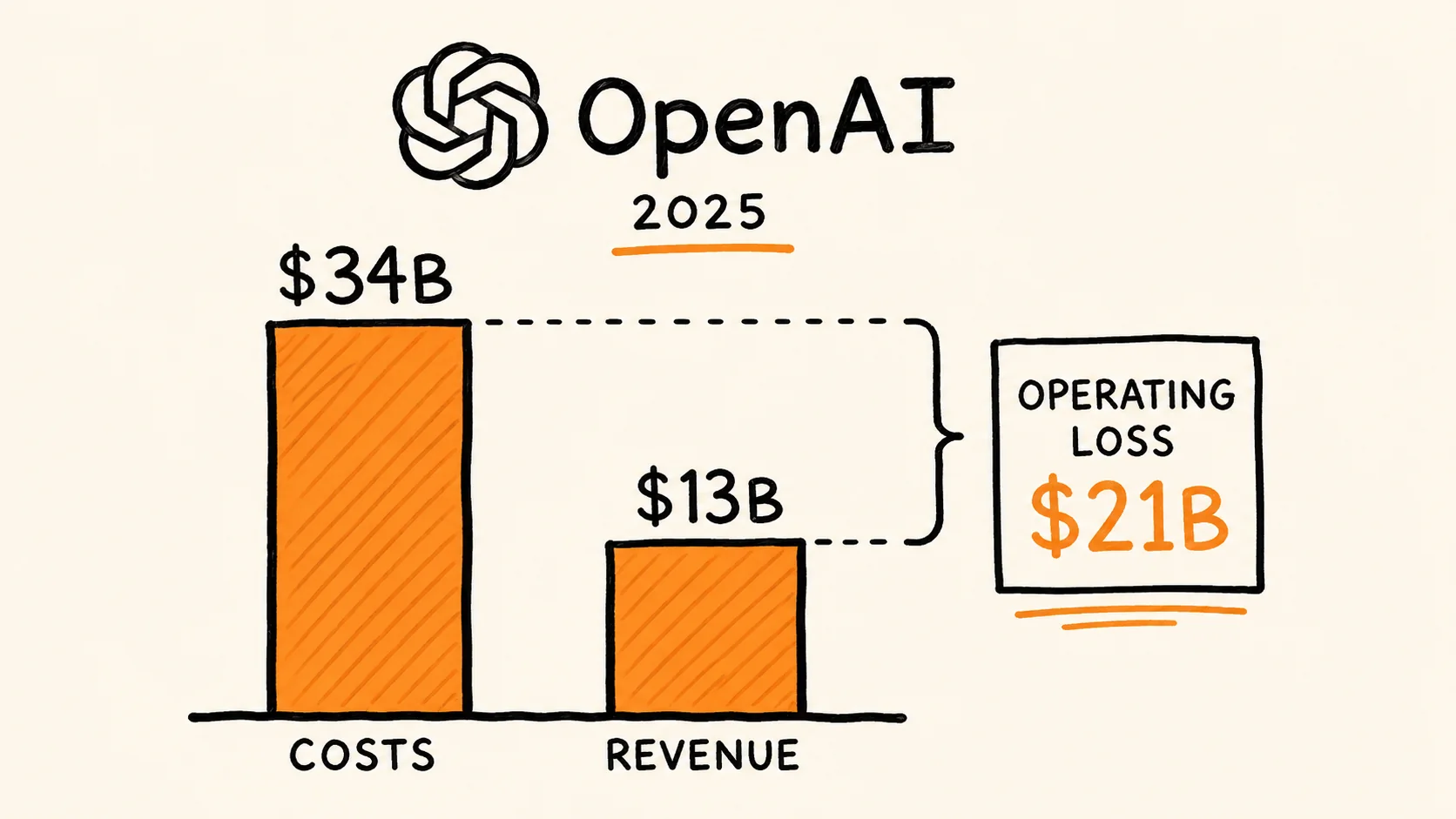

What OpenAI's 2025 Numbers Actually Show

The financial picture behind the subsidy became clearer after internal OpenAI documents were reported by journalist Ed Zitron in 2026. The figures he published have not been verified against a public filing or audited statement; they are presented here as reported.

According to those documents, OpenAI generated $13.07 billion in revenue in 2025, against total costs and expenses of $34 billion. The resulting operating loss was $20.92 billion. A separate, larger figure — a net loss attributable to the company of $38.53 billion — reflects additional accounting effects tied to the organization's conversion from a non-profit to a for-profit structure, including fair value adjustments on convertible interests and warrant liabilities worth roughly $41.55 billion. The two numbers measure different things and should not be used interchangeably.

What is unambiguous in the reported figures is the scale of sales and marketing expenditure. OpenAI reportedly spent $5.73 billion — equivalent to 44 percent of its total revenue — on sales and marketing in 2025. Zitron's accompanying analysis contextualizes this alongside evidence of flatlining corporate enterprise adoption, characterizing it as spending required to sustain demand that was not growing organically.

The company closed 2025 with just over $50 billion in assets, with roughly half in cash. Against a $34 billion annual cost base, that runway is finite — particularly with large capital commitments ahead and no public market yet from which to raise equity.

The four cards below summarize the key reported figures from OpenAI's 2025 financials.

The 2026 Pricing Pivot and Its Immediate Effect on Enterprise Buyers

The theoretical affordability problem became a practical pricing crisis in the first half of 2026. Two developments made that concrete.

In April 2026, leaked internal Microsoft documents — covered in Rosenthal's June 2026 analysis — revealed that GitHub Copilot's week-over-week operational costs had nearly doubled since January, forcing Microsoft to pause new sign-ups for student and paid individual tiers and tightly restrict rate limits. The company moved to redirect users toward token-based billing, ending the predictable flat-rate model it had previously used to drive adoption.

Anthropic made a parallel shift in May 2026, transitioning customers to token-based pricing. The practical effect on enterprise clients was immediate and severe. Corporate buyers — small business CEOs among them — reported spending jumps of as much as 7 times their previous monthly bill on the first day of the new pricing structure, according to reporting referenced by Rosenthal. The behavior that had previously been a liability for the platform (high token consumption) became a visible line item for the customer overnight.

The broader business press — Bloomberg, Scott Galloway, and Tom's Hardware among others — shifted coverage framing in the same period toward what Rosenthal describes as an "AI cost panic," with enterprise purchasers increasingly aware that the usage patterns their employees had normalized under subsidized pricing were unsustainable under token billing.

The timeline below maps the key events from the first public warning through the enterprise pricing shock of mid-2026.

What the timeline makes visible is that the repricing was not a sudden strategic pivot. The math was flagged publicly in September 2023. The capital commitment kept growing anyway. The companies now absorbing 7-times bill increases are paying the delayed cost of a model that was always dependent on subsidy — they just weren't the ones being subsidized.

The next pressure point is the IPO pipeline. OpenAI, Anthropic, and SpaceX are all expected to seek public market capital, each carrying significant cash burn. Public market investors will require a credible margin story. The subsidy era made the addressable market look large. The repricing era will test whether that market was real.

China Taps Its $28 Trillion Capital Markets to Fund an AI Race With the US

CXMT's 500%-plus Shanghai debut made it China's top listed firm, capping Beijing's shift from subsidies to stock and bond markets to fund its AI buildout.

Europe's Debt Pile Is Nearing €1 Trillion. It's Still Not a Safe Asset

EU bonds are AAA-rated and near €1 trillion, but a 50-basis-point spread over German Bunds explains why a true European safe asset still doesn't exist.

US Economy Grows a Sluggish 1.5% in Q2 as Inflation Stays Stuck Near 3.7%

Commerce Department data show Q2 GDP grew 1.5%, below forecasts, as PCE inflation eased to 3.7% and three Fed officials pushed for a rate hike.

The Middle-Income Trap, Explained: Why Only 34 Economies Have Escaped Since the 1990s

108 economies are stuck in the "middle-income trap," per the World Bank. Here's what the trap is, how South Korea escaped it, and what's holding Vietnam back.

Comments (0)

Please sign in to join the discussion.

No comments yet.

Be the first to share your perspective on this topic.